Oil prices rebound from one-month low after Trump’s tariff threat

[ad_1]

Jean-Paul Pelissier | Reuters

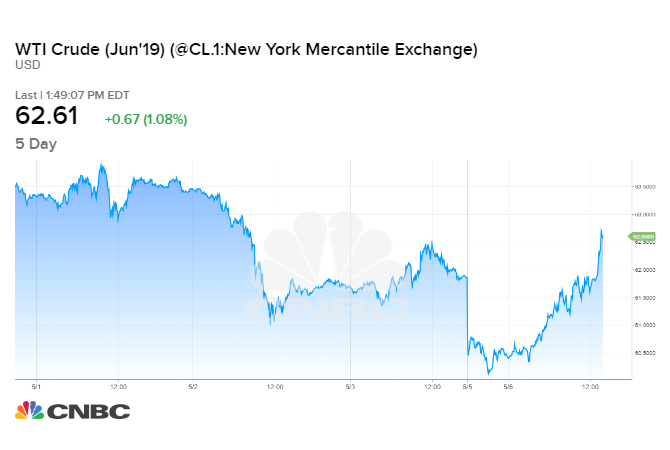

Oil futures edged higher in volatile trade on Monday as rising tensions between the United States and Iran buoyed prices, which earlier touched a one-month low after U.S. President Donald Trump said he may raise tariffs on Chinese goods.

U.S. West Texas Intermediate crude futures settled 31 cents higher at $62.25 per barrel on Monday. WTI hit $60.04 earlier in the session, its lowest since March 29.

Brent crude futures rose 46 cents to $71.31 per barrel around 2:30 p.m. ET (1830 GMT). Brent earlier hit its lowest since April 2 at $68.79.

Additional buying was sparked after WTI broke through $62 a barrel in early afternoon trade, said Bob Yawger, director of energy futures at Mizuho in New York.

Injecting risk premium into the market, the United States is deploying a carrier strike group and a bomber task force to the Middle East to send a clear message to Iran that any attack on U.S. interests or its allies will be met with “unrelenting force,” U.S. national security adviser John Bolton said on Sunday.

“You’re seeing those increasing geopolitical tensions,” said Phil Flynn, an analyst at Price Futures Group in Chicago.

The deployment comes after the Trump administration tightened energy sanctions on Iran last week in a bid to drive the Islamic Republic’s oil exports to zero. The U.S. stopped issuing sanctions waivers that allow some of Iran’s biggest customers to import limited amounts of Iranian crude oil.

Elsewhere, top oil exporter Saudi Arabia raised its crude oil prices for June to its Asian and European customers, and cut prices to the United States, a signal that Riyadh is in no hurry to boost oil supply ahead of an OPEC meeting next month.

Also pressuring the market, Trump said on Twitter on Sunday that tariffs on $200 billion of goods would increase on Friday to 25 percent, reversing his February decision to keep them at 10 percent due to progress in trade talks.

Trump early on Monday appeared to defend his Sunday statement, citing the trade deficit between the United States and China. “Sorry, we’re not going to be doing that anymore!” he tweeted.

The comments worried investors about trade talk progress between the world’s two largest economies and ignited concerns that ongoing tensions could hurt global oil demand.

China’s Foreign Ministry spokesman Geng Shuang told a news briefing on Monday that a Chinese delegation was still preparing to go to the United States for trade talks.

“We are also in the process of understanding the relevant situation,” he said.

Within the oil industry, U.S. crude production has surged by more than 2 million barrels per day since early 2018 to a record 12.3 million bpd. The United States is now the world’s biggest oil producer, ahead of Russia and Saudi Arabia.

However, that growth has largely stalled this year due to pipeline bottlenecks in the Permian Basin, the largest U.S. shale field. Oil production fell by nearly 200,000 barrels per day in February, data from the Energy Information Administration showed last week.

American drillers have also been focusing on improving their finances, rather than growing production at any cost.

The number of rigs drilling for oil in the United States rose by two to 807 in the week to May 3, data from oil services firm Baker Hughes showed on Friday. The count is down by 70 rigs since the start of the year.

— CNBC’s Tom DiChristopher contributed to this report.

Source link