US plan to choke off Iran oil exports casts uncertainty over market

[ad_1]

A gas flare on an oil production platform in the Soroush oil fields is seen alongside an Iranian flag in the Gulf.

Raheb Homavandi | Reuters

The United States sharply tightened energy sanctions against Iran on Thursday, seeking to cut the Islamic Republic’s exports to zero and ushering in a new era of uncertainty for the oil market.

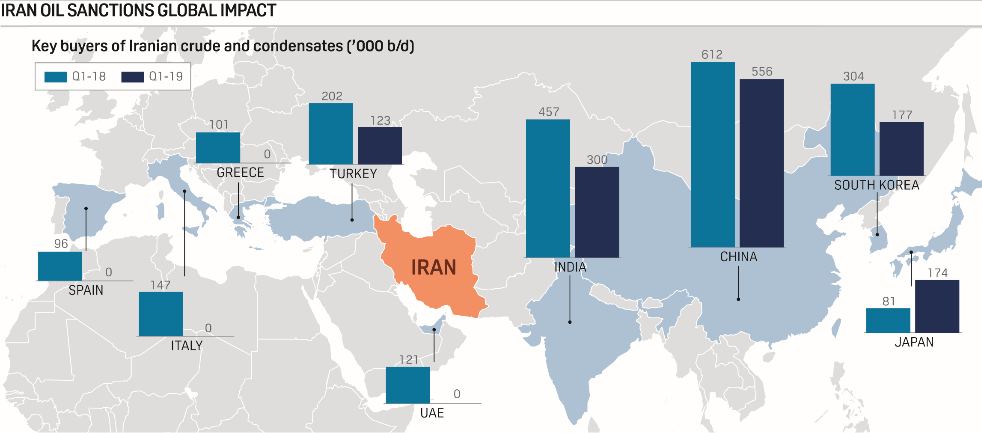

President Donald Trump restored Obama-era sanctions against Iran last year but granted waivers to eight nations, allowing them to import limited quantities of Iranian crude. Last week, his administration surprised the market by announcing it would not extend the waivers.

Investors and analysts expected Trump to tighten the waivers every six months, allowing China, India, Turkey and other importers to gradually wind down purchases of Iranian crude.

The sudden move to cut off Iran’s exports threatens to wipe out much of the shipments, which have recently totaled more than 1 million barrels per day, or roughly 1% of global consumption. To fill that gap and prevent fuel costs from spiking, Trump has turned to his allies in Saudi Arabia, the world’s top oil exporter.

Iran’s oil buyers, source: S&P Global Platts

But the Saudis have not made firm commitments and continue to consider extending a six-month deal to limit output with OPEC and other producers. That is raising concerns about a period of tighter supply and higher oil prices.

“President Trump’s decision to zero out waivers for importers of Iranian oil on May 2 represents an audacious act of oil brinkmanship as the strategy of keeping prices contained now rests almost exclusively on Saudi Arabia’s willingness to open the taps amid accelerating global supply outages,” Helima Croft, global head of commodity strategy at RBC Capital Markets, said in a recent research note.

Oil prices initially jumped to six-month highs after Trump revoked the waivers, with international benchmark Brent crude hitting $75.60 and U.S. crude rising to $66.60. Prices were trading around $71 and $62, respectively, on Thursday.

Tight oil market creates risk

Analysts say the tighter sanctions alone will not cause a supply shock, but they make the oil market more vulnerable to a shortage that sends fuel costs higher.

That is in part because oversupply in the oil market is draining, and supply and demand are coming into balance. Some analysts even think the market is slightly undersupplied.

At the same time, supply disruptions and threats of further outages are widespread.

U.S. sanctions on Venezuelan oil giant PDVSA have accelerated a plunge in the country’s oil output. In Libya, renewed conflict between rival leaders has put the OPEC nation’s oil supplies at risk. Nigeria, Africa’s largest producer, has also suffered one of its periodic outages.

In Europe, contaminated oil sent by pipeline from Russia has disrupted supplies to refineries in several nations.

Meanwhile, OPEC and its allies, including Russia, are still trying to keep 1.2 million bpd off the market.

The Saudi factor

Trump is putting pressure on the Saudis and OPEC to reverse course, but many analysts are skeptical the so-called OPEC+ alliance will comply.

The group hiked output ahead of U.S. sanctions on Iran in November, only to be surprised when Trump granted the import waivers. The flood of OPEC oil and weaker-than-anticipated sanctions contributed to a collapse in Brent from $86 to $50 a barrel and prompted producers to agree in December to cut output.

Saudi Arabia needs oil prices around $80 a barrel to balance its budget. The country’s influential oil minister, Khalid al-Falih, has hedged his statements since Trump’s announcement on sanctions waivers, stressing that the kingdom will respond to shortages.

That signals the Saudis are wary of another pre-emptive supply hike, says Bill Farren-Price, a geopolitical risk analyst at RS Energy Group.

“Saudi Arabia feels that the cuts deal of December was hard fought and quite an achievement and they don’t want to throw the baby out with the bathwater and lose those price gains in the pursuit of policy that frankly could work badly against them, as it did last year,” he said.

Still, the country is pumping about 500,000 bpd below its quota under the OPEC deal, so the Saudis could raise production and still keep the OPEC+ deal in place. The group meets June 25-26 to discuss extending the agreement.

Sanctions beaters

Also offsetting the oil price impact, few analysts expect Iran’s exports to actually fall to zero.

Some of Iran’s oil will probably be smuggled through neighboring Iraq or sold in non-dollar-denominated transactions to skirt U.S. sanctions, says Tamar Essner, director of energy and utilities at Nasdaq Corporate Solutions. She estimates 800,000-900,000 bpd of Iran’s 1.3 million bpd in exports could come off the market.

But the biggest challenge will be securing buy-in from China, Iran’s biggest customer, says RBC’s Croft. Beijing fiercely opposes the U.S. sanctions.

She believes Chinese refiners will cut purchases by a couple thousand barrels per day, but will keep importing some Iranian crude. Turkey is also a wildcard, and could maintain about half of its current purchases, she says.

Source link